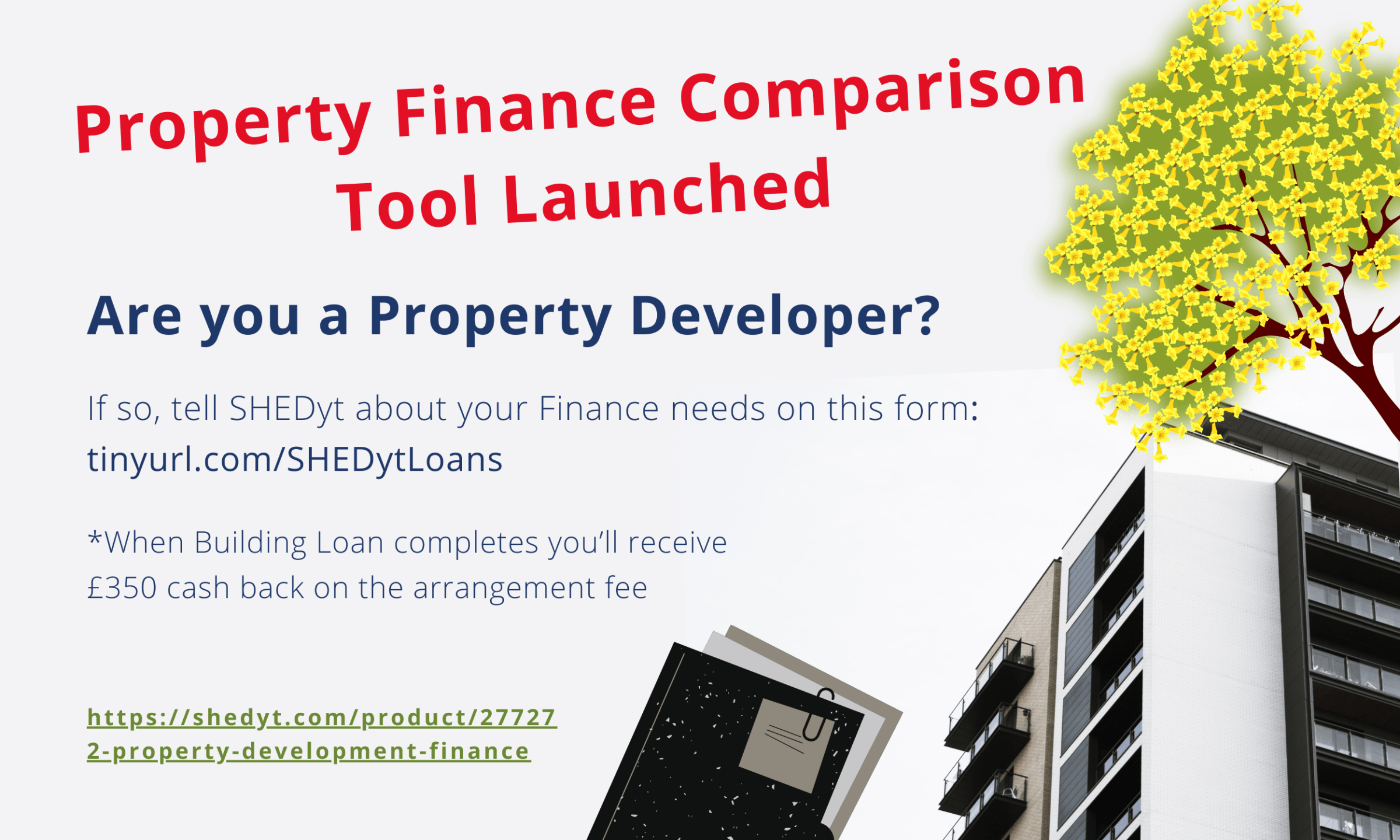

Case Study of Exit Finance

In the previous blog, the SHEDyt team discussed the value of 'Exit Finance' and how it can be leveraged to benefit your Property Development business.

Background

In this second Exit Finance article we explore an example from September 2024 where a landlord required refinancing of a ground-up build nearing completion of two detached houses and intended to pay back the original loan post-sale funds. Although the business had secured initial development finance to fund the project, work was remaining as the end of the loan term approached and they were about to be charged default interest as funds were only going to arrive on completion.

Financing options

The home builder had two refinancing options (A) too extend the term with the existing lender or (B) to explore more flexible deals with other lenders.

As a starter, the existing lender offered a three-month extension with a 2% fee. However, the client needed more favourable terms with greater flexibility, recognising that three months might not be enough to finalise construction, market the properties, and close the sales.

Instead, the House Builder chose a specialist 'Exit Finance' solution that gave them additional time and borrowing flexibility to complete a project. In this scenario, it allowed the client to remain in control of the timeline without added pressure from another tight refinancing deadline and the lender taking into account the project was mostly complete.

Project Details

- Investment Route: Limited company

- Project Scope: Construction of two detached houses

- Borrowing Requirement: 75% loan-to-value (LTV) with a flexible repayment timeline to cover:

(1) Finalising the build, (2) Marketing the properties with an agent & (3) Completing sales to fund loan repayment

Typical Challenges

Securing development finance requires a well-defined exit strategy and lenders typically look for clear repayment plans, especially in cases where sale proceeds are expected to cover the loan a the end of the terms. However, a flexible loan term was essential to accommodate the time needed for effective marketing and selling.

The Solution - Key features of the loan included

- No exit fees

- Early repayment option if the sales were completed ahead of schedule

- Lending based on market value rather than a “30-day valuation,” maximising the client’s borrowing potential.

Loan Summary

- Property Value: £1,200,000

- Gross Loan Amount: £900,000

- (LTV) Loan-to-Value: 75%

- Monthly Rate: 0.81%

- Term: 12 months

- Payment Basis: Retained interest

This case study highlights how Development Exit-Finance can support Developers by providing both the time and financial resources to complete projects on their terms, maximising the potential for profitable sales; If you’re interested in learning more about the value of Exit Finance and no-obligation consultation, then use this product link Development Exit Loans for Property Developers or book a meeting here > goldentrust.youcanbook.me

Disclaimer: This information is not financial, tax, or legal advice. Mortgage and loan rates are subject to change.

Make Your Business Online By The Best No—Code & No—Plugin Solution In The Market.

30 Day Money-Back Guarantee

Say goodbye to your low online sales rate!